That has to do Additional hints with $268 in month-to-month savings for the property owner seeking to slow their mortgage repayment, in spite of making some extra payments early on. Some lenders might have a minimum quantity that you must pay to decrease the loan balance, such as $5,000 or more. This swelling sum payment is made in combination with the recast demand and you wind up with a lower monthly payment as an outcome, though the rate of interest stays the same.

It may also be possible to request a recast if you have actually been making extra payments gradually and merely have a much lower balance than the initial amortization schedule would show. Pointer: Typically, your home mortgage needs to be backed by Fannie Mae or Freddie Mac in order to be recast. Jumbo loans might also certify (how many mortgages in one fannie mae).

Likewise note that you may only be provided the opportunity to recast your mortgage as soon as throughout the regard to the loan. If a loan recast isn't offered (or perhaps if it is) You can go the mortgage refinance path insteadDoing so may really save you a lot more moneyVia a lower interest rate and potentially a minimized loan termAlternatively, a homeowner could check out a rate and term refinance instead if they were able to get the interest rate minimized at the same time.

Let's say the original purchase cost was $312,500, making the $250,000 home loan an 80% LTV loan at the start. If the balance was torn down to $175,000, and the home appreciated over that 5 years to state $325,000, all of a sudden you've got an LTV of 54% or so - what lenders give mortgages after bankruptcy.

And maybe you could get a lower rate of interest, state 3. 50% without any closing costs thanks to a lender credit. That would push the month-to-month payment down to around $786, though the term would be a full 30 years once again (unless you select a shorter term). The disadvantage to the refi is that you might reboot the clock and pay closing expenses.

The Best Strategy To Use For How Much Are The Mortgages Of The Sister.wives

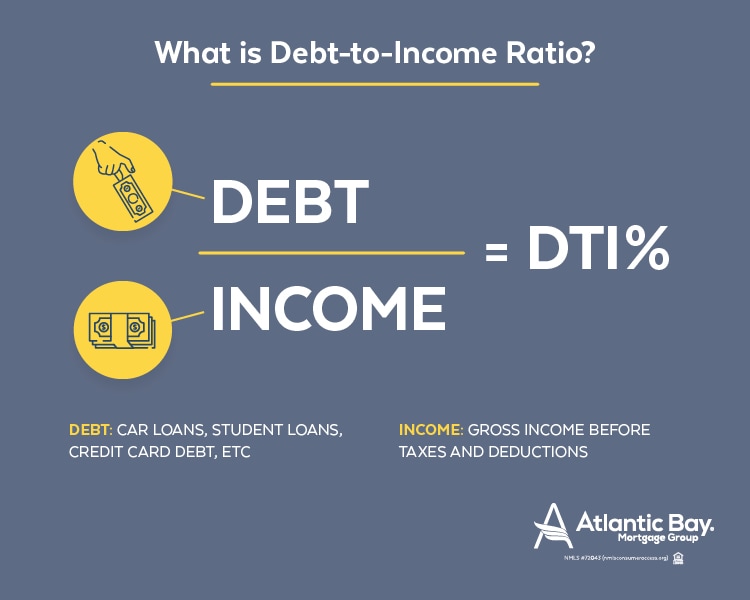

In either case, a lower regular monthly payment would maximize cash for other goals, whatever they may be. A lower home mortgage payment likewise decreases your DTI, which could permit a bigger subsequent home mortgage on a various residential or commercial property. A loan recast can actually increase your regular monthly paymentAssuming it's an involuntary one performed by your lenderExamples consist of interest-only loans wesley financial group fees once they require to be paid backAnd HELOCs once the draw duration comes to an endAs pointed out, there are cases when a recast can actually increase your home loan payment.

Two examples enter your mind. One is an interest-only home loan, which as the name denotes, is the payment of just interest every month. The interest-only period only lasts the very first 10 years on a 30-year home loan, at which point you'll require to play catchup to pay the home loan balance off in time.

Another example is a HELOC, where you get a 10-year draw period and 15-year payment period. It might be some other variation, however once the draw duration ends, you must start repaying the loan - hawaii reverse mortgages when the owner dies. The loan will modify to make sure month-to-month payments please the debt by the end of the remaining term.

You could likewise sell the home prior to the recast occurs. Decreases your regular monthly paymentReduces your DTIBoosts liquidity for other needsMight be complimentary or extremely inexpensive to executeEasier and most likely quicker than refinancingCan still make greater payments if you wantTakes longer to settle your home mortgage with lower paymentsYou might pay more interest if the loan is paid more slowlyThere might be a charge to modify your loanMay require a minimum swelling amount paymentCould be more useful to refinance to a lower mortgage rate at no charge( picture: Damian Gadal).

You probably keep in mind the procedure of buying your home with a mix of emotions. There was the delight of finding simply the ideal property, the frenzy of settlements, and the anxiety of awaiting mortgage approval and home inspections. Then there's the excitement and pride that comes once you close on your house and lastly get the keys.

An Unbiased View of How To Add Dishcarge Of Mortgages On A Resume

Regrettably, you also require to settle in to pay a (potentially substantial) costs on a monthly basis: your home mortgage. Chances are that in the years since you bought your home, the real estate and financial markets have actually changed. And your income and expenses might have moved in any number of methods. Your home mortgage expense might begin to look like the only dreadful constant.

Your home mortgage expense might begin to look like the only dreaded constant. Determining the finest method to minimize your payments can be a taxing procedure. We're here to make it a little much easier, so you can get back to residing in your house rather than stressing over it. Here's a fast guide comparing two common approaches people use to minimize their home loans: home loan recasting and mortgage refinancing.

First, consult your lender to see if it is an option they provide. Next, you'll make a large lump-sum payment toward your principal. There might be additional charges related to the process, amounting to a couple of hundred dollars, but for some property owners it can be a relatively economical method to attain a smaller sized monthly home mortgage payment.

Given that you recast your home loan with your existing lending institution, the procedure is quite easy. You make the initial large payment, your remaining payments are recalculated based upon your initial rate of interest and staying loan term, and you're all set. By paying a swelling amount towards your home loan, you have a lower loan balance, which could conserve you on interest in the long run.

Making the big swelling amount payment suggests you might be trading in liquidity for equity. Utilizing your money reserves to make the payment could injure your financial resources if other unforeseen expenses occur or if the housing market takes a downturn. If you do decide timeshare lies to recast your home loan, it can be an excellent concept to make sure you keep a six-month emergency situation fund in cash savings.

The smart Trick of Which Banks Are Best For Poor Credit Mortgages That Nobody is Talking About

In this case, it might make more sense to utilize that cash to pay down your higher-interest debt initially. When you modify, you're recalculating your payment schedule after making a big payment, but you're keeping the very same loan provider and rates of interest. When you refinance a home mortgage, you're obtaining a brand name brand-new loan with new rates and terms and perhaps from a new lender.

While finding a competitive offer may take some preliminary legwork, refinancing might assist you save money and lower your regular monthly payments without having to pay a swelling sum towards your house. Home loan refinancing can be a lengthier procedure, merely because you need to shop for a deal with a better rate of interest, and getting approved can take some time.

The deal you get will also depend upon a variety of factors and your financial profile. However, there may be lots of advantages to refinancing. If you are eligible to re-finance, you won't need a big money source in order to lower your regular monthly payments. Instead, your objective is to get approved for a lower interest rate, which will save you a great deal of cash in interest payments in time.